m. stanfield@resetbasis

Dec 13, 2025

19 tweets

Tired of losing money in real estate?!

Today, we’re going to look at a pitch deck from Nitya Capital. I’ll teach you a few things that you can hopefully use to separate good deals from bad ones.

Buckle up.

First, let’s get some hand-waving CYA bullshit out of the way. I am not an LP in any Nitya deals, and I have nothing to gain if their company is successful or a failure.

Second, these slides were mass-emailed by one of their presumably disgruntled LPs, and a friend of a friend passed them along to me. Neither I nor anyone I know has signed any kind of NDA.

Third, I’m going to steer clear of saying, “this is wrong” and instead suggest a bunch of questions I might ask if they approached me for money.

With that crap out of the way, let’s chop it up.

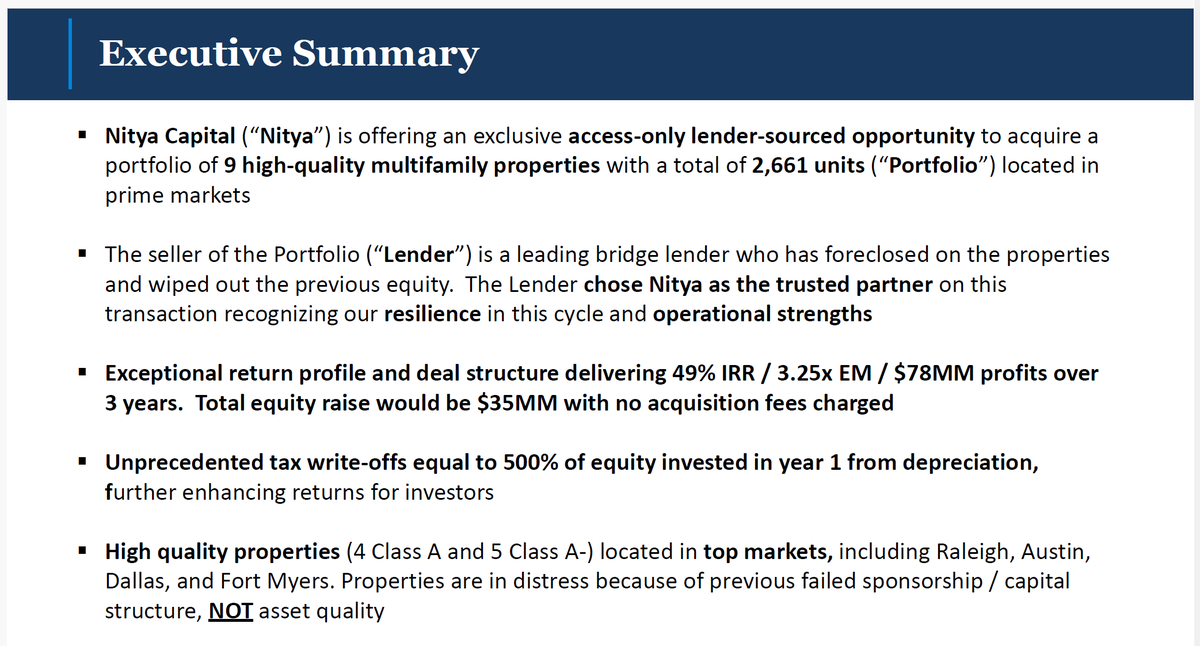

- The third bullet point should immediately set off a bunch of alarms in your head. Tripling your money in three years obviously sounds compelling, but those returns are atypical for multifamily. So, I would hope this presentation covers the significant risks associated.

- Depreciation is nice, but it's not free money. Ask your CPA about depreciation recapture.

- When someone blames the last owner and says the deals are in good shape, that's potentially true, but not always true. Hop on Google Earth, look at street view, and see how the properties look to you.

Multifamily investing isn't that complicated. If the building looks like shit on the outside, it's gonna look like shit on the inside. GPs fix curb appeal before air handlers and roofs.

- A discount to extreme peak pricing in 2022 is not convincing by itself. You should ask for recent sales comps to help you get comfortable with the basis.

Also, it looks like exiting at the prior peak generates a 2.5x not a 3.25x, so the plan is to sell above peak pricing in three years. Does that sound reasonable to you? Are interest rates going back to 1%?

- Third bullet. Didn't take long to find the risk. They're taking on 92.5% leverage, which is highly unusual in multifamily and not something I would be comfortable with. You should ask for a sensitivity table if the equity was cut down to 65-75% and see if the returns are still attractive. Leverage does not make a bad deal good.

- You aren't any more aligned with the lender than the bear tamer is with the bear. If this works, the lender is reasonably happy. If it doesn't, they'll keep the equity you put into the deal to lower their UPB, foreclose, and try this same stunt with the next group.

It's totally fine to have the lender as a partner, just be aware of what you're doing. It's not alignment, and it's not a feature.

- 2nd bullet. I know I said I wouldn't say, "this is wrong", but this is wrong. By their own admission on webinars and in investor letters, Nitya has significant problems in their portfolio. The assertion that they haven't had a loss is dishonest. They may not have sold anything at a loss yet, but that doesn't mean the losses aren't on the books.

Lots of GPs, big and small, are having issues, not singling Nitya out, but this type of hubris needs to be addressed.

- 3rd bullet. No. Just no. These deals have been sloshing around the market for years. LoanCore (lender) has been trying to find someone to bail them out for a very long time.

Shit, I've toured 6 of these deals personally. We were interested in buying them off GVA, but realized quickly they were worth less than the debt and dropped them.

I'm proud to say in mid-2024, I offered LoanCore 70% of par, which they found offensive.

I can't speak to exactly why they picked Nitya, but the lender is a debt fund trying to make money. Those guys typically pick the group that says the biggest number. Nothing proprietary about this game.

Let's assume you don't have any fancy real estate software and you're curious about the data presented on this slide.

First, I would look at the assertion that all of these are Class A properties, despite most being built in the 1980s, and ask myself, "does that feel true to me?"

Here's some pictures of 4804 Haverwood. Does that look like Class A housing to you, Mrs. Investor?

Here's some pics of Copper Mill, and the beautiful neighborhood retail next door.

I own a property down the street; nothing about Rundberg is Class A.

And here's Solara. You get the idea.

Going back to the overview slide. One of the bullet points says "extremely low future supply," which I know isn't true because I do this for a living, but you presumably do not.

So, I'd suggest a simple Google search. Do any of the names match?

You can make money in high supply markets, just good to understand if what you're being told in the deck lines up with your view of the market.

The overview slide also says, "robust tenant demand," and you should see if that's true.

In a weak market, apartments offer move-in incentives and discounts called "concessions." First, I'd check the website of the apartments you're considering investing in. Are they offering concessions? The three deals we looked at above are.

I would also Google concessions and see what comes up. See if the top markets for concessions in the country are the ones you're being pitched.

If so, does that feel like robust tenant demand to you?

Here's a market slide. As with all things, verify the assumptions. I won't pick them all apart, you get the idea, but if you Google "Fort Myers Apartment Supply," the first article you see is this one.

costar.com/article/189136

In my opinion, that doesn't seem to line up with the GP's statement that Fort Myers has a low supply pipeline.

Again, you can make good money in soft markets; these aren't bad deals for that reason alone. My concern is that the tone of the deck seems to be trying to support a value-add narrative, and that just feels thin to me.

Ask for sale comps. The assumption that you can sell all of these deals for the same price as the prior peak in three years makes me nervous.

I'm wrong more often than I'm right, so perhaps that's the case here, but these feel like big prices to pay for these properties.

Here, they break down one of the deals they are buying. They sold it to GVA at the peak and are buying it back. A compelling pitch to most LPs, but you gotta ask more questions.

A thing I like to do on short hold periods (and three years is short) is ask myself, "what else could I buy today for my assumed exit price per unit?"

Well, here's an interesting data point. This property, Ascend at Pioneer Hill traded for less than 200k per unit a few months ago.

It was built in 2024 and looks like this. How comfortable are you that your 1980s-built property is going to trade for 175k per unit in 3 years after seeing this?

- There's nothing LBO about this; don't let people try to wow you with fancy finance terms. They're using a ton of leverage, that's it.

Leverage at this level freaks me out, but you are free to do what you like.

I would ask for another sensitivity table showing how far off plan they can be for rents/expenses before they have to start doing capital calls. 92.5% leverage doesn't leave much room for error.

You should also ask how quickly the lender can foreclose and what could trigger that happening.

I want you to look at these two slides, ignore the noise, and notice two things.

First, the interest rate on the loan is SOFR+2.75% (see first slide). Most of this week, SOFR was around 4%, so you're looking at ~6.75% interest.

Second, the stabilized yield on cost they are optimistically projecting is 6.06% (bottom left second slide). They are doing a lot of work, and still stabilizing at negative leverage. What?!

Look, some people are smarter than me and take on negative leverage during their rehab period, and perhaps they carry negative leverage through the hold and still make money. But I've never seen it work.

Also, they're assuming an exit at a 4.68 cap. You'll be surprised when I tell you this, but you can buy the nicest property in almost any city in the US right now for a 4.68 cap. So, why would someone pay that cap rate for 1980s-built multifamily?

Well shit, this ain't great.

Their plan is to stabilize occupancy to 95%, which is above market in most/all of these locations. Second, they plan to increase rents 20% over three years. In markets where rents have been dropping faster than anywhere in the country.

They don't have a big value add plan here either. According to the prior slide, they're only investing $6,800 per unit in a mix of upgrades and presumably some deferred maintenance.

Here's roughly how much in-unit upgrades cost in these markets.

New Appliances - $2,000

Granite Countertops - $1,800

Flooring - $1,200

Paint - $750

New cabinets (front only) - $2,200

Lighting - $500

If your plan is to increase rents by hundreds of dollars a month, what upgrades do you have planned? How much of the $6,800 goes to deferred maintenance and systems?

If the portfolio is currently 73% occupied, how much will it cost to get those vacant units rent-ready?

Look at the total portfolio yield on cost. They are paying a 3.75% cap for this distressed portfolio! Call any broker you know and ask what you can buy for a 3.75 cap right now. It will be new, gorgeous, and fully stabilized. Why the hell would you pay that yield for some distressed, older multifamily that you need to fix? You just don't have to do that.

And I know I said this already, but why in gods name do you think you're going to exit at a 4.68 cap?!

I'm out of space and time, so I'll close with this.

When thinking about investing in workforce housing, which this stuff absolutely is, you need to understand who your customer is and what they want.

The majority of renters in these apartments are focused on price first. They have a tight budget, and every dollar has a job. Would they like granite countertops and stainless steel appliances? Sure. Are they willing/able to pay you a premium for that stuff? No.

If rent goes from $1,200 to $1,500, they move out. And the people who can pay $1,500 have better buildings to choose from and better neighborhoods in which to live.

The biggest mistake syndicators made in the last run up was conflating general rent growth do to a lack of supply, with a desire to pay more for housing. Now that supply has exploded, the workforce renter has options and will be heavily focused on price.

Be careful out there.

Missing some tweets in this thread? Or failed to load images or videos? You can try to .