1/ What is $STRC and how it fuels the $MSTR rocket  With mNAV is compressed, Saylor found a way to raise money without diluting shareholders

With mNAV is compressed, Saylor found a way to raise money without diluting shareholders

With mNAV is compressed, Saylor found a way to raise money without diluting shareholders

2/ Strategy has built something that doesn't really exist anywhere else in capital markets: a variable rate perpetual preferred stock that functions as a continuous BTC acquisition engine

It's called $STRC. And it's moving serious volume.

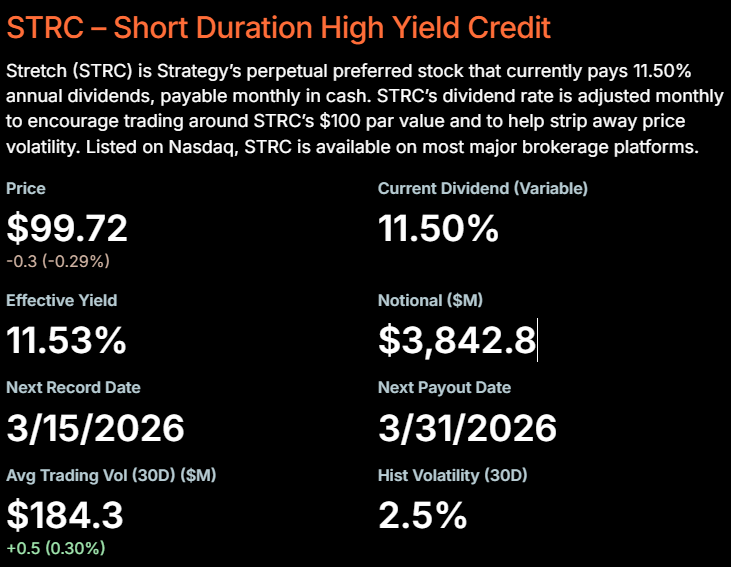

3/ STRC is a variable-rate perpetual preferred stock. Buy it at ~$100, collect a monthly dividend (currently 11.5% annualized), and Strategy will use the proceeds to buy Bitcoin

The stock is propped up by a dividend of 11.5%, up from 9% at launch

4/ There's alot of trust involved. Strategy has sole discretion over every dividend adjustment. They can abandon the peg entirely if needed

The dividend also requires alot of cash. If MSTR equity ATM can't fill the hole, Strategy may have to use its $2.25B cash reserve

5/ STRC sits inside a capital stack that amounts to a Bitcoin-backed yield curve:

MSTR → common equity, leveraged BTC proxy

STRK → 8% fixed preferred, convertible

STRF → 10% fixed preferred, cumulative

STRD → 10% non-cumulative preferred

STRC → 11.5% variable, monthly, price-pegged

6/ We've seen some pretty impressive numbers so far

Week of March 2–8: ~$377M raised through STRC. Combined with common equity issuance, Strategy acquired 17,994 BTC that week at ~$70,946 avg

March 10: $180M in STRC proceeds in one session — 567% of daily mined BTC supply

7/ This is a strategic move. STRC lets Strategy raise billions without touching MSTR shareholders' BTC-per-share. The dividend is an operating cost, staying away from equity dilution

In a compressed mNAV environment, preferred issuance is the only accretive path

8/ Remember that reflexivity works in reverse

If BTC drops hard enough to compress mNAV, STRC demand weakens, dividends need to rise to hold the peg, and cash burn accelerates

9/ So far it's working. But it's a system built on confidence, and the controls are entirely one-sided

We're watching for cracks in the form of reduced dividends

Missing some tweets in this thread? Or failed to load images or videos? You can try to .